Most venture structures focus on quick exits, leaving long-term value on the table. You know that aligning ownership, governance, and incentives is crucial—but the path is often unclear. This post lays out a clear framework for venture structure alignment that supports durable growth and real impact. For further insights, you can explore this resource on value creation strategies.

Structuring Ventures for Lasting Success

Creating a solid venture structure is key to achieving lasting success. It involves careful planning and strategic alignment at every stage. Your venture's structure should support growth, stability, and meaningful impact. Let's explore how to design such a structure.

Ownership and Cap Table Design

Ownership lays the foundation for any venture. Understanding your cap table is crucial. It shows who owns what and how much. It's a simple tool that can prevent conflicts. A balanced cap table can drive collaboration.

First, consider equitable distribution. Founders, early employees, and investors should feel valued. This fosters commitment and trust. Second, transparency is vital. All stakeholders should understand their share. This clarity avoids misunderstandings. For more tips, explore best practices for cap table design.

Ownership ties closely to control. Founders need enough control to guide their vision. Yet, investors seek some influence to protect their interests. Finding this balance ensures strategic decisions align with long-term goals. A well-structured cap table aligns interests and supports growth.

Governance Frameworks for Startups

Governance defines how decisions are made. In startups, it's often overlooked. But the right framework can propel success. It sets the rules for decision-making and accountability.

Start with a clear governance structure. Define roles and responsibilities early. This avoids power struggles and confusion. Next, establish decision-making processes. They should be flexible yet structured. Allow room for innovation while ensuring accountability. Learn more about effective governance in this comprehensive guide.

Communication is a pillar of good governance. Regular meetings and updates keep everyone informed. They also foster a culture of openness and trust. A sound governance framework supports your venture's vision and long-term success.

Incentives and Vesting Plans

Incentives motivate your team to perform their best. They align individual goals with the company's vision. A well-designed incentive plan can drive growth and loyalty.

Start with clear goals. What behaviors and outcomes do you want to reward? Tailor incentives to these goals. Equity is a powerful motivator. It gives employees a stake in the company's success. For effectiveness, implement a vesting schedule. It ensures commitment over time. Here's how vesting and incentive plans can enhance alignment.

Remember, incentives are not just financial. Recognition and development opportunities also matter. They can boost morale and retention. Ensure your incentive plan is fair and transparent. It should reflect contributions and promote shared success.

Strategic Investment Programs

Investing strategically can take your venture to new heights. It involves more than just providing capital. It's about smart allocation and value creation. Let's delve into strategic investment programs.

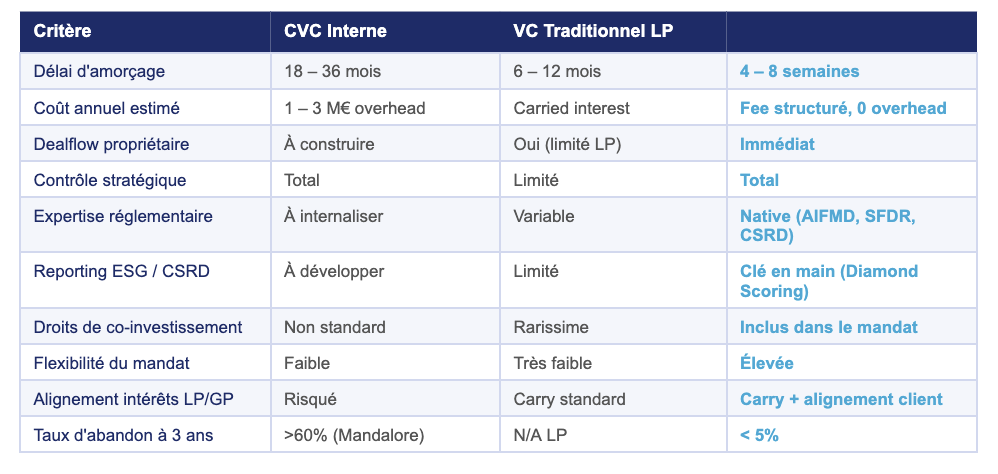

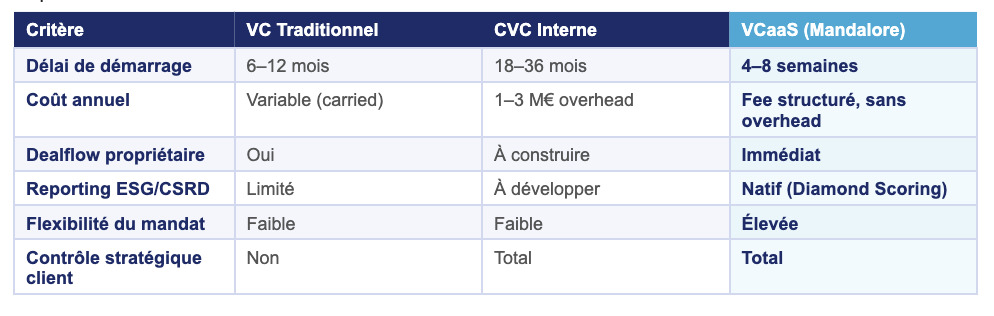

Corporate Venture Capital Insights

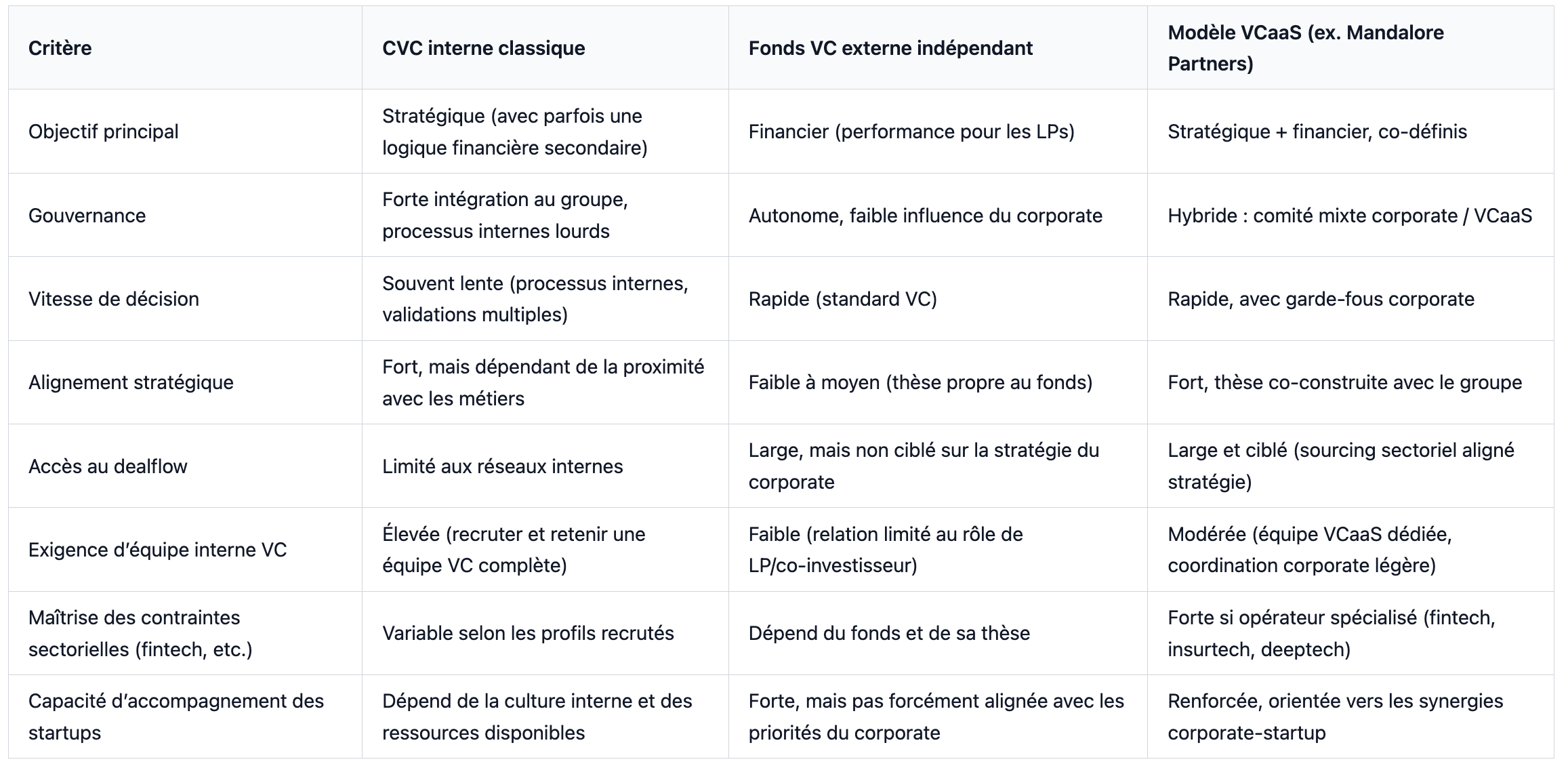

Corporate venture capital (CVC) offers a unique advantage. It combines financial investment with strategic benefits. CVC can drive innovation and market expansion. But it requires a clear strategy.

Start by aligning investments with your corporate goals. CVC should complement your core business. Next, foster collaboration between your venture and corporate teams. This synergy can enhance outcomes. To see examples of successful CVC, check out these case studies.

CVC can also provide valuable industry insights. It connects you with emerging trends and technologies. This knowledge can guide strategic decisions. A well-executed CVC program fuels growth and innovation.

Co-Investment Syndication Explained

Co-investment syndication involves pooling resources with other investors. It spreads risk and increases access to deals. This collaborative approach can amplify results.

First, identify compatible co-investors. Look for those with similar goals and values. Second, establish clear agreements. Define roles, contributions, and returns. This clarity prevents conflicts. For more details, review this co-investment guide.

Co-investment can also enhance your network. It connects you with partners and opportunities. These relationships can lead to future collaborations. Co-investment syndication is a powerful tool for strategic growth.

Financing Strategy and Liquidation Preferences

A sound financing strategy is essential for success. It determines how you raise and allocate funds. It also addresses investor expectations and returns.

First, plan your funding rounds. Determine how much you need and when. This foresight prevents cash flow issues. Next, consider liquidation preferences. They dictate how proceeds are distributed. Understanding these terms is crucial for founders and investors alike. Explore more about financing strategies and their impact.

Transparency is key in financing. All parties should understand the terms and expectations. Open communication builds trust and prevents disputes. A robust financing strategy supports sustainable growth.

Building Effective Partnerships

Partnerships can amplify your venture's impact. They provide resources, expertise, and market access. Building effective partnerships is vital for long-term success.

Board Governance Best Practices

Board governance shapes your venture's direction. It ensures effective oversight and decision-making. Good governance drives success and mitigates risks.

Start with a diverse board. Different perspectives can spark innovation and solutions. Define clear roles and responsibilities. This clarity prevents overlaps and conflicts. For deeper insights, explore board governance best practices.

Regular evaluations are crucial. They assess board performance and effectiveness. Constructive feedback fosters improvement. Effective board governance guides your venture toward its goals.

Operational Excellence with KPIs

Operational excellence is key to scaling. Key Performance Indicators (KPIs) measure progress and guide actions. They align operations with strategic goals.

Select relevant KPIs for your venture. They should reflect core activities and outcomes. Regular monitoring ensures you stay on track. Adjust as needed to meet evolving needs. For more on KPIs, check this detailed resource.

Operational excellence requires teamwork and commitment. Foster a culture of continuous improvement. Encourage feedback and innovation. This focus enhances efficiency and growth.

Impact Measurement and Portfolio Acceleration

Impact measurement tracks your venture's social and environmental contributions. It's crucial for responsible growth. Portfolio acceleration enhances impact and returns.

Define clear impact objectives. They should align with your mission and values. Use metrics to track progress. This data guides decisions and strategies. For impact measurement examples, see this insightful guide.

Portfolio acceleration involves targeted support. It boosts venture performance and impact. This approach maximizes value for all stakeholders. Impact measurement and acceleration drive meaningful change.

In summary, structuring ventures for lasting success requires careful planning and strategic alignment. From ownership and governance to investments and partnerships, each element plays a crucial role. By focusing on these areas, you can create a robust framework that supports durable growth and real impact.